Business in Perspective

chief financial officer review of 2022 performance

An Overview

The Kingdom being recognised as the world’s fastest growing economy by 8.7% in 2022 with a positive outlook for 2023 laid the stage for Al Rajhi Bank to continue delivering a strong performance across all business lines. Guided by its 2021-2023 Bank of the Future (BOTF) Strategy and its initiatives, Al Rajhi Bank recorded a 22% YoY growth across its balance sheet. Consumer spending continued its positive trend with an increase of 9.5% in 2022 on the back of improved economic activities across the Kingdom. The financing portfolio also grew at 26% for the year to reach SAR 568 Bn.

Mortgage recorded a growth of 30% YoY, and now represents close to 39% of our total financing portfolio and 51% of the Al Rajhi retail book. In addition, the successful implementation of our BOTF Strategy saw a 57% growth in our corporate book and an equally impressive 61% growth in our SME business, contributing to a significant 59% YoY growth of our non-retail book. We also delivered a solid net income growth of 16% YoY to reach SAR 17.2 Bn., driven by both a 9% increase in net yield income, and a non-yield income growth of 20%.

One of the key highlights for Al Rajhi Bank in 2022 was our successful diversification of funding sources, with our Treasury Group carrying out three major transactions during the year under review; a Tier 1 Sukuk was issued for the first time in Al Rajhi Bank’s history at a total value of SAR 6.5 Bn., the Bank also became the first Islamic Bank in the world to raise a Sharia-compliant, green syndicated loan of USD 1.2 Bn., and also went on to announce a Tier 1 Sukuk public issuance, the first of its kind in the market, raising the issue to SAR 10 Bn. to meet the demand of over 125,000 investors.

A detailed review of Al Rajhi Bank’s results of operations and financial position is given below:

Five-year summary of the Income Statement

| Description | 2022 SAR ‘000 |

2021 SAR ‘000 |

2020 SAR ‘000 |

2019 SAR ‘000 |

2018 SAR ‘000 |

| Income | |||||

| Gross financing and investment income |

28,201,631 | 21,441,506 | 17,377,963 | 16,962,583 | 14,993,709 |

| Return on customers’, banks’ and financial institutions’ time investments | 6,028,944 | 1,049,570 | 464,946 | 534,860 | 506,724 |

| Net financing and investment income | 22,172,687 | 20,391,936 | 16,913,017 | 16,427,723 | 14,486,985 |

| Fee from banking services, net | 4,624,140 | 3,933,107 | 2,659,680 | 1,987,367 | 1,867,034 |

| Exchange income, net | 1,162,162 | 787,898 | 783,894 | 774,096 | 755,804 |

| Other operating income, net | 616,030 | 603,457 | 364,669 | 295,278 | 209,695 |

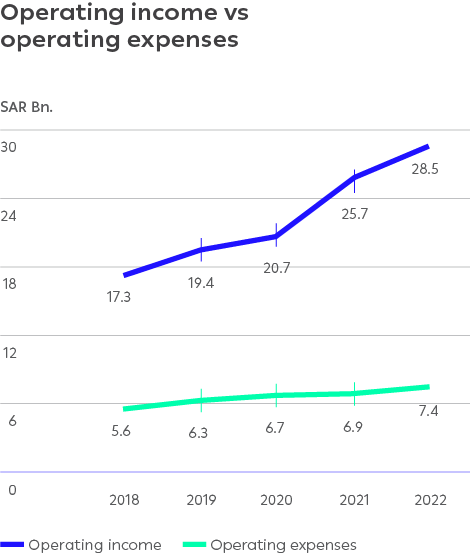

| Total operating income | 28,575,019 | 25,716,398 | 20,721,260 | 19,484,464 | 17,319,518 |

| Expenses | |||||

| Salaries and employees’ related benefits | 3,395,191 | 3,132,346 | 2,977,344 | 2,794,046 | 2,809,449 |

| Rent and premises related expenses | 0 | 0 | 0 | 314,567 | |

| Depreciation and amortization | 1,330,119 | 1,141,932 | 1,118,148 | 1,059,582 | 603,136 |

| Other general and administrative expenses | 2,725,760 | 2,652,244 | 2,646,409 | 2,532,213 | 1,925,518 |

| Operating expenses before credit impairment charge | 7,451,070 | 6,926,522 | 6,741,901 | 6,385,841 | 5,652,670 |

| Impairment charge for financing and other financial assets, net | 2,001,259 | 2,345,086 | 2,165,740 | 1,772,265 | 1,530,946 |

| Total operating expenses | 9,452,329 | 9,271,608 | 8,907,641 | 8,158,106 | 7,183,616 |

| Income for the year before Zakat | 19,122,690 | 16,444,790 | 11,813,619 | 11,326,358 | 10,135,902 |

| Zakat for the year | (1,971,865) | (1,698,579) | (1,218,071) | (1,167,831) | (6,367,949) |

| Net income for the year | 17,150,825 | 14,746,211 | 10,595,548 | 10,158,527 | 3,767,953 |

| Revenue breakdown by subsidiaries | 2022 SAR ‘000 |

| Al Rajhi Capital Company – KSA | 866,520 |

| Management and Development for Human Resources Company – KSA | 947,953 |

| Al Rajhi Bank – Kuwait | 88,892 |

| Al Rajhi Bank – Jordan | 147,927 |

| Tuder Real Estate Company – KSA | 187,952 |

| Al Rajhi Corporation Limited – Malaysia | 233,625 |

| Emkan Finance Company – KSA | 1,053,064 |

| Tawtheeq Company – KSA | 9,443 |

| Al Rajhi Financial Markets Ltd | – |

| International Digital Solutions Co. (Neoleap) – KSA | 346,766 |

| Ejada System Limited Co. – KSA | 248,805 |

| Total | 4,130,948 |

Total operating income

Al Rajhi delivered a strong growth in total operating income driven by both yield and non-yield income to reach SAR 28.6 Bn. for 2022, recording a growth of 11% YoY. Yield-based income for the year grew 9% to SAR 22.2 Bn., accounting for 78% of the Bank’s total operating income.

The continued focus on increasing our revenue mix resulted in the Bank’s non-yield income increasing to represent 22% of the Bank’s total operating income. Non-yield income growth was driven by a 18% fee income increase YoY; the positive migration to cashless payments coupled with an increase in consumer spending as well as an increase in market share (from acquired businesses) resulted in growing payment revenues during the year under review. A decent YoY growth in trade and cash management fee income from the steadily growing corporate business also contributed to the revenue mix. Exchange income has also shown a strong performance increasing by 48% YoY.

Operating expenses

The Bank’s operating expenses for the year amounted to SAR 7.5 Bn., an increase of 7.6% resulting from the 22% YoY growth of our overall balance sheet, and higher transaction volume compared to last year. The Bank continued to make strategic investments during the reporting period to execute and deliver ambitious KPIs of the BOTF Strategy.

However, the Bank recorded a 11% increase in operating income, resulting in a strong, 354-basis-point positive jaws, and a 86-basis-point cost-to-income improvement. This ensured Al Rajhi Bank recorded the leading cost-to-income ratio in the local market, standing at 26.1% for the period.

Impairment Charges

In line of the International Financial Reporting Standard 9 – Financial Instruments (IFRS 9) issued by the International Accounting Standards Board (IASB), Al Rajhi Bank updated the “expected credit loss” (ECL) framework for the recognition of impairment, taking into consideration current events and forecast information including the positive macro outlook for The Kingdom. This resulted in our net impairment charges for the period to decrease to SAR 2 Bn., almost a 15% drop YoY. These lower charges complemented by the growth of our financing portfolio resulted in our cost of risk decreasing from 0.60% in 2021 to 0.39% in 2022.

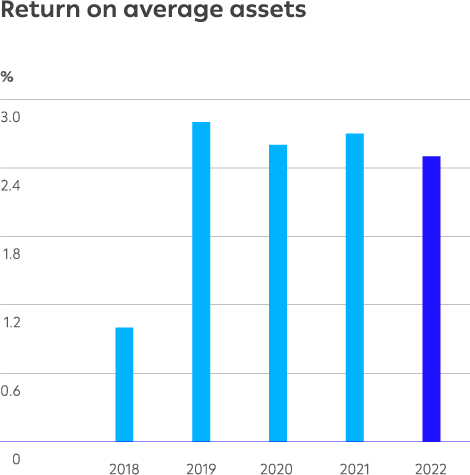

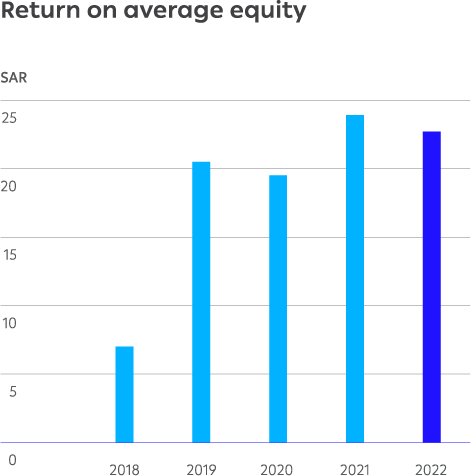

Profitability

Having recorded SAR 17.2 Bn. in net income after Zakat for the year, Al Rajhi continued to maintain industry-leading returns, with a steady Return on Assets (ROA) at 2.46% and Return on Equity (ROE) at 22.68% in 2022. The Bank also recorded a 3.71% return on its risk-weighted assets (RORWA) at the end of the year.

Five-year summary of the statement of financial position

| Description | 2022 SAR ‘000 |

2021 SAR ‘000 |

2020 SAR ‘000 |

2019 SAR ‘000 |

2018 SAR ‘000 |

| Cash and balances with Central Bank | 42,052,496 | 40,363,449 | 47,362,522 | 39,294,099 | 43,246,043 |

| Due from banks and other financial institutions, net | 25,655,929 | 26,065,392 | 28,654,842 | 32,058,182 | 32,387,760 |

| Investments, net | 102,146,142 | 84,433,395 | 60,285,272 | 46,842,630 | 43,062,565 |

| Financing, net | 568,338,114 | 452,830,657 | 315,712,101 | 249,682,805 | 231,758,206 |

| Investment properties, net | 1,364,858 | 1,411,469 | 1,541,211 | 1,383,849 | 1,297,590 |

| Property and equipment, net | 11,338,782 | 10,665,799 | 10,234,785 | 10,407,247 | 8,649,435 |

| Other assets, net | 11,469,701 | 7,874,467 | 5,033,990 | 4,417,764 | 3,629,245 |

| Total Assets | 762,366,022 | 623,644,628 | 468,824,723 | 384,086,576 | 364,030,844 |

| Dues to banks and other financial institutions | 70,839,117 | 17,952,140 | 10,764,061 | 2,219,604 | 7,289,624 |

| Customers’ deposits | 564,924,688 | 512,072,213 | 382,631,003 | 312,405,823 | 293,909,125 |

| Other liabilities | 26,377,182 | 26,338,711 | 17,311,141 | 18,269,492 | 14,526,229 |

| Total liabilities | 662,140,987 | 556,363,064 | 410,706,205 | 332,894,919 | 315,724,978 |

| Equity | |||||

| Share capital | 40,000,000 | 25,000,000 | 25,000,000 | 25,000,000 | 16,250,000 |

| Statutory reserve | 29,287,706 | 25,000,000 | 25,000,000 | 21,789,632 | 16,250,000 |

| Other reserves | (427,569) | 282,107 | (134,728) | (216,041) | (349,555) |

| Retained earnings | 9,864,898 | 16,999,457 | 8,253,246 | 868,066 | 12,499,171 |

| Proposed dividends | 5,000,000 | 0 | 0 | 3,750,000 | 3,656,250 |

| Equity attributable to shareholders of the Bank | 83,725,035 | 67,281,564 | 58,118,518 | 51,191,657 | 48,305,866 |

| Tier 1 Sukuk | 16,500,000 | 0 | 0 | 0 | 0 |

| Total equity | 100,225,035 | 67,281,564 | 58,118,518 | 51,191,657 | 48,305,866 |

| Total liabilities and equity | 762,366,022 | 623,644,628 | 468,824,723 | 384,086,576 | 364,030,844 |

Assets

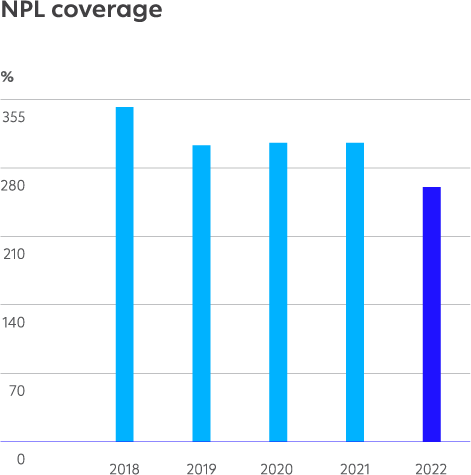

Al Rajhi Bank passed the SAR 700 Bn. milestone in total assets during the reporting period, closing the year with assets amounting to SAR 741 Bn., a 27% growth YoY. The Bank’s asset quality continued to be the best in the market with 97.5% of our financing portfolio recognised as stage 1 assets. Stage 2 and stage 3 assets stood at 1.7% and 0.8% of the financing portfolio respectively, with coverage ratios for stage 3 standing at 64%, stage 2 at 18% and stage 1 at 0.58%, all higher than market average. Our prudent risk management continued to be reflected in our NPL ratio which was the lowest in the market, reducing from 0.65% in 2021 to 0.54% in 2022, the fourth consecutive year of improvement for this KPI. Additionally, the Bank’s NPL coverage ratio too, lead the banking sector at a healthy 260%.

Deposits and other liabilities

Total liability of Al Rajhi Bank stood at SAR 662 Bn., a YoY increase of 19%. Customer deposits increased by SAR 53 Bn. during the year under review, a growth of 10% YoY to reach SAR 565 Bn., with demand deposits making-up almost 64% of total customer deposits. Time deposits also recorded a strong growth in 2022, increasing by SAR 72 Bn. YoY. Interbank borrowing increased by SAR 53 Bn., which also included a SAR 4.4 Bn. of USD syndicated green loan considered to be the largest Sharia-compliant syndication in the Middle East.

Stability

With a strong balance sheet backed by market-leading asset quality and NPL ratio, healthy regulatory liquidity position and comfortable levels of capital ratios, Al Rajhi Bank successfully maintained its steady growth and consistent performance, demonstrating the stability, shareholder loyalty and creditworthiness of the Bank.

Capital

Al Rajhi Bank continued to maintain a strong capitalisation profile above regulatory minimum requirements with a Core Equity Tier 1 (CET1) ratio of 17.0% and a total capital adequacy ratio of 21.4%, marginally higher than the ratios recorded in 2021. A 17% YoY increase in Risk-Weighted Assets (RWA) arising primarily from growth in the financing portfolio led to 18% increase in Credit Risk RWAs, impacting our capital ratios. However, a decrease in RWA density from 68.2% in 2021 to 65.3% in 2022 demonstrated the Bank’s improving risk quality of assets. The reporting period saw the Bank focused on strong internal capital generation to help support the capital position of the Bank, while also exploring new business opportunities.

Liquidity

Al Rajhi Bank’s liquidity position remained healthy and within the regulatory requirements, with a regulatory Loan-to-Deposit Ratio (LDR) of 85.9% in line with our internal optimised level. The Bank’s Net Stable Funding Ratio (NSFR) and Liquidity Coverage Ratio (LCR) stood at comfortable levels at 110% and 126% respectively, and above statutory minimum requirement. Al Rajhi Bank recorded a 25% YoY growth of High Quality Liquid Assets (HQLA) amounting to SAR 118 Bn., as at 31 December 2022.

| Geographical analysis of the total income of the bank and its subsidiaries | 2022 SAR ‘000 |

| KSA | 29,342,624 |

| Middle East and East Asia | 470,444 |

| Total | 29,813,068 |

![]()

Future outlook

Al Rajhi Bank will continue to focus on delivering BOTF strategy KPIs, with our key focus steady on the Bank’s core business franchise across retail, corporate and SME segments, capturing new business opportunities given the positive outlook of the Saudi economy. The implementation of BOTF strategy will support the Bank to optimise synergies across the Bank’s subsidiaries, and nurture a financial ecosystem that will provide our loyal customers with rapidly evolving financial solutions to address their ever-changing needs.