Context

operating context

The International Monetary Fund (IMF) recorded 3.4% growth in the world in 2022 driven by better-than-expected performance of advanced economies. 2023 will see 2.9% growth before rising to 3.1% in 2024 driven by “surprisingly resilient” demand in the United States and Europe, easing energy costs and the reopening of China’s economy, but limited by the rise in central bank rates. High inflation, rising energy prices, a geopolitical crisis and supply chain disruptions around the globe defined a near-tumultuous year, leading to much uncertainty and trepidation in markets worldwide.

However, despite the grim global outlook, Gulf Cooperation Council (GCC) countries fared well in the reporting period, with individual GCC economies expanding significantly by the end of the year. The Kingdom of Saudi Arabia in particular reported a 8.7% growth in 2022 fuelled by rising oil prices and a boom in economic activity, driving profits for financial institutions in the region, monetary tightening notwithstanding.

Al Rajhi Bank, one of the world’s largest Islamic banks, skilfully navigated global headwinds that threatened to destabilise entire markets while contending with challenges faced regionally and locally during 2022, coming out on top as an industry behemoth in the MENA region.

Global trends

With global growth slowing from 6.0% in 2021 to 3.4% in 2022, fear of a global recession loomed large as the year came to a close; a period rife with rising inflation and high cost-of-living, both of which had a significant impact on banks around the world. Unexpected inflation hurt lenders due to the decline in purchasing power of their money during the life of the loan, and banks, as net monetary creditors, would decrease the value of their nominal assets due to rising prices that let the value of their nominal liabilities diminish.

Higher prices reduced consumer purchasing power in 2022, giving rise to lower demand for credit. This slowdown in credit growth resulting from lower consumer confidence and deferred investments from corporates and influenced the price of assets, thereby decreasing their net to value.

The Ukraine crisis and other unforeseen geopolitical developments led to friction in trade relations and supply chain disruptions not observed in years. With over USD 100 Bn. of Russian debt held by foreign banks, concerns were raised about the risks posed to banks outside Russia and the potential for a default to trigger a liquidity crisis similar to the one that occurred in 2008. Banks faced stress tests from the impact of energy crisis defaults in the wake of the conflict, with the potential of higher energy prices resulting in higher costs for consumers and industries, translating to reduced cash flows to fund their financial engagements.

Towards the end of the reporting period, the bear market in stocks was intensifying as forecasted. Mortgage rates globally had more than doubled, corporate credit spreads were widening, and the value of the dollar was soaring against most currencies.

Growing debt in developing nations during the reporting period exposed banks with large holdings of sovereign debt to losses, with government finances coming under pressure, leading to the decline of government debt market value. This forced banks — especially those with less capital — to curtail lending to companies and households, further slowing economies, adding more pressure on government finances, and further squeezing banks.

Central banks around the world rushed to tighten their monetary policy in the face of near-runaway inflation and fast-depleting forex reserves. New investments were halted as governments across the world attempted to contain fiscal deficits by controlling expenses, and normalising supply chains.

Apart from such regulatory changes, the global financial sector also continued to be impacted by the drive towards digitalisation as well as the demand for sustainable financing during the year under review.

Regional trends

Against a backdrop of global economic upheaval, GCC economies recorded notable levels of expansion in 2022, with the Kingdom of Saudi Arabia outperforming developed nations as well as emerging economies to become the world’s fastest growing economy in 2022, registering a growth rate of 8.7% for the year.

Regional Central Banks increased their interest rates following the US Fed monetary tightening policy due to GCC currencies being pegged to the USD. However, GCC countries maintained lower levels of inflation than the rest of the world in 2022, benefiting from the ability to provide lower energy prices to their citizens. Subsidies supported by surpluses in fiscal balance further eased inflationary pressures.

A regional-level warming to a less hydrocarbon-dependent, diversified economic model opened up new possibilities for a more sustainable growth strategy during the reporting period, as the world becomes increasingly forced to transition into a low-carbon economic environment.

2022 was also notable for increased profitability levels of banks across the GCC region, with many banks recording profits higher than pre-pandemic levels. The key drivers of this profit boom were fiscal stimulus by the government and spending backed by higher oil prices, which in turn supported the expansion of economic activity. The cost of risk stabilized by returning to normalized levels by the second half of the year, offset by higher net interest margins as well as adequate provisioning. Lending growth of GCC banks accelerated in 2022 compared to 2021 due to greater economic activity and improving sentiment based on high oil prices.

Local trends

The Kingdom’s impressive growth in 2022 was supported by proactive structural and fiscal reforms that were implemented within the framework of its deeply ambitious and comprehensive Vision 2030 strategy, which set a strong foundation for a diversified economy and enhanced the growth in non-oil sectors at sustainable rates over the medium-term.

The Government of Saudi Arabia, through Ministry of Finance and Saudi Central Bank (SAMA), took several steps to contain inflation during the reporting period such as capping energy prices, introducing SAR 20 Bn. support package, applying fiscal discipline, and increasing repo and reverse repo rates, which enabled the Kingdom to control local inflation despite global inflationary pressures.

The Kingdom continued to attract more foreign investment flows through Vision 2030 Programmes and new investment opportunities across multiple sectors. Vision 2030 megaprojects such as AMAALA, Green Riyadh, NEOM, Qiddiya, ROSHN and The Red Sea project continued to expand the Kingdom’s economic, social, technological and cultural diversification at an impressive scale during 2022. Meanwhile the push for non-oil sector investments saw focus shift towards diverse industries, from Aerospace and Defence, Transport and Logistics, and Food and Agriculture, to Metals and Mining, Utilities and Renewables, Consumer Goods and Retail as well as Financial Services, with the Kingdom’s scheduled launch of Open Banking services in 2023.

Commercial and industrial real estate continued to see benefits of economic growth, as well as the relocation of offices of international firms into Saudi Arabia, a direct impact of the investment opportunities unlocked by Vision 2030.

The Kingdom’s Saudisation agenda continued steadily in 2022, with more women being integrated into the workforce. This was evidenced by the Kingdom’s first place ranking in labour force growth rate among the G20 countries during 2012 – 2021, according to a recent report published by the National Labour Observatory.

The public sector also continued to fast adapt to international labour market demands in competency and productivity supported by the rapid digitalising of services, nurturing a competent labour market with a stronger value proposition for private sector partnering.

The Public Investment Fund (PIF) and the National Development Fund (NDF) – the financial arms of the government – continued to play an important role in supporting regular events of the calendar year return back to pre-pandemic levels, including Hajj, Umrah, the Saudi Seasons, and tourism in general.

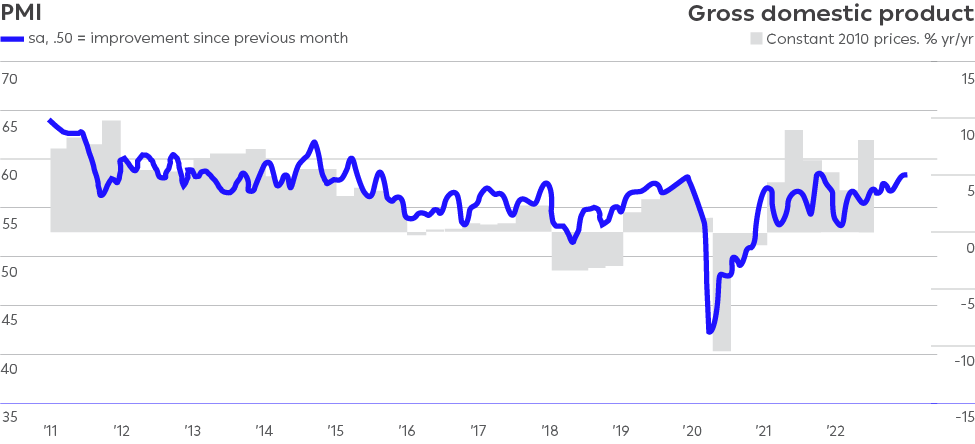

S&P Global – a leading global provider of credit ratings, benchmarks and analytics, in the Riyad Bank Saudi Arabia Purchasing Managers’ IndexTM (PMI®) at the end of December, recorded an increasing headline index of 56.9, signalling the ongoing marked expansion of the Kingdom’s non-oil private sector economy. Growth was underpinned by strong gains in both output and new orders, whilst firms continued to bolster their purchasing activity.

The December 2022 Primary Consumer Sentiment Index (PCSI) showed that the Saudi Arabia’s IPSOS PCSI was 70.3, reaching the top of the global list. The score for the reporting period peaked at 71.3 in June.

Sector-specific trends

During 2022, the Saudi banking sector supported the implementation of Vision 2030 projects and Vision Realisation Programmes (VRPs), contributing towards enhancing investments and stimulating projects across multiple sectors, while also giving rise to the contribution of domestic content.

The budget for 2022 released by the Saudi Ministry of Finance indicated economic recovery as a key pillar for the year’s fiscal outlook, with expansion expected to help support the budget position and debt levels as a portion of GDP. The Kingdom’s banking sector identified a number of key focus areas in line with Vision 2030, including Mortgage, Tourism, and Transport and Logistics.

Beyond the conventional risks, the Kingdom’s banking sector was also impacted by a number of emerging risks in 2022; these included cyber risk due to the intensifying financial activity online; digitalisation risk due to potential inadequacies in digital transformation; fintech risks in rapidly growing and aggressively competitive open banking environment; and long-term asset risks rising from declining value of fixed rate assets.

Despite a number of challenges, Saudi Banks witnessed robust growth in profitability in 2022 underpinned by higher total interest income and lower impairment charges, resulting in a return on assets (RoA) of 1.99%. Industry wide loan-to-deposit ratio (LDR) continued to increase during the year, with the sector also exhibiting improvement in cost efficiencies stemming from growth in operating income, resulting in an improving cost-to-income (C/I) ratio.

Increased interest rates continued to feed the Saudi banks’ margins. Credit to the private sector expanded due to growth in mortgage owing to market saturation, and a Vision 2030-backed increase in demand for corporate credit. However, heightened liquidity pressures stemming from faster credit growth than expected will lead banks to find alternative source of funding since liquidity will be a key driver in credit growth in 2023.

Due to this year’s strong performance, Saudi banks are touted to enter an uncertain 2023 on solid footing, with the expected slowdown of the global economy, compounded by potential liquidity constraints.