An overview

Immediate and controlled action from the onset of the pandemic in 2020 by the Saudi Government ensured minimum impact on the local economy and rapidly improving economic recovery and activity during 2021. Following the strong results from its successful “ABCDE – Back to Basics strategy” (2016 – 2020), Al Rajhi Bank swiftly adopted the new three-year Bank of the Future (BOTF) Strategy in 2021 as the Kingdom and the world recovered from the pandemic, and focused on delivering and executing its strategic goals across all banking functions based on four pillars; build on the core, outperform the market, transform technology and fulfil more customer needs.

With the underlying priority of elevating the customer experience, the Bank recorded a strong performance across all segments of the business in 2021; retail banking expanded its digital offering across personal finance, auto finance and mortgage to successfully retain its market leadership position, increasing efficiencies, reducing turn-around times and recording unprecedented double digit growth. Corporate banking saw the expansion of its product portfolio to include financing, cash management, trade and hedging products, increasing its market share by gaining deeper insight into customer needs through the Customer Relationship Management (CRM) system and 360o client coverage model. Al Rajhi also realigned its SME business with its BOTF strategic goals, revamping the segment with new products and end-to-end digital capabilities; from online account opening to Point of Sales (POS) and financing requests through the Kingdom’s currently top-ranked business mobile app.

Additionally, the Bank seamlessly integrated its subsidiary services to build a comprehensive, multi-service banking and financing ecosystem, optimising the synergies across the Group so that customers can benefit from brokerage and investment banking, microfinancing, digital payments and other services. During the year under review, we continuously monitored our Net Promoter Score (NPS) to ensure our initiatives to improve customer engagement and customer experience were successful, ending the year with the top NPS in the Kingdom.

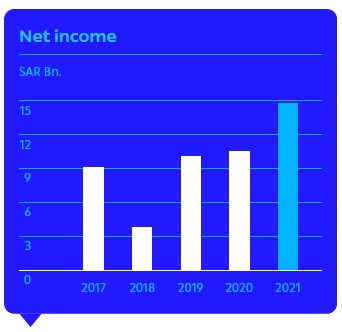

The BOTF strategy contributed immensely to the delivery of strong results in 2021. We recorded SAR 14.7 Bn. in net income after Zakat for the year, a phenomenal 39% growth over 2020 compared to the 4.3% growth rate recorded the previous year. Total assets grew to SAR 624 Bn. as at 31 December 2021, recording a year-on-year growth of 33%, largely driven by exceptional growth in financing (43%) and investment (40%) portfolios. Customer deposits grew by 34% to SAR 512 Bn., funding 82% of the total asset base.

A detailed review of Al Rajhi Bank’s results of operations and financial position is given below:

Income Statement

The Bank recorded a net income of SAR 14.7 Bn. in 2021, with the improved financial metrics reflecting the disciplined implementation and accelerated achievements of Al Rajhi’s strategic goals and objectives under its new BOTF strategy.

Five-year summary of the Income Statement

| Description | 2021 SAR ‘000 |

2020 SAR ‘000 |

2019 SAR ‘000 |

2018 SAR ‘000 |

2017 SAR ‘000 |

| Income | |||||

| Gross financing and investment income | 21,441,506 | 17,377,963 | 16,962,583 | 14,993,709 | 12,581,004 |

| Return on customers’, banks’ and financial institutions’ time investments | 1,049,570 | 464,946 | 534,860 | 506,724 | 551,587 |

| Net financing and investment income | 20,391,936 | 16,913,017 | 16,427,723 | 14,486,985 | 12,029,417 |

| Fee from banking services, net | 3,933,107 | 2,659,680 | 1,987,367 | 1,867,034 | 2,697,208 |

| Exchange income, net | 787,898 | 783,894 | 774,096 | 755,804 | 841,839 |

| Other operating income, net | 603,457 | 364,669 | 295,278 | 209,695 | 336,390 |

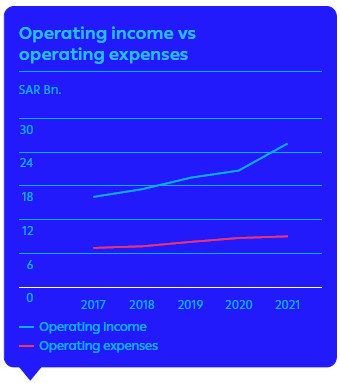

| Total operating income | 25,716,398 | 20,721,260 | 19,484,464 | 17,319,518 | 15,904,854 |

| Expenses | |||||

| Salaries and employees’ related benefits | 3,132,346 | 2,977,344 | 2,794,046 | 2,809,449 | 2,813,918 |

| Rent and premises related expenses | – | – | – | 314,567 | 311,025 |

| Depreciation and amortization | 1,141,932 | 1,118,148 | 1,059,582 | 603,136 | 440,566 |

| Other general and administrative expenses | 2,652,244 | 2,646,409 | 2,532,213 | 1,925,518 | 1,671,052 |

| Operating expenses before credit impairment charge | 6,926,522 | 6,741,901 | 6,385,841 | 5,652,670 | 5,236,551 |

| Impairment charge for financing and other financial assets, net | 2,345,086 | 2,165,740 | 1,772,265 | 1,530,946 | 1,547,577 |

| Total operating expenses | 9,271,608 | 8,907,641 | 8,158,106 | 7,183,616 | 6,784,128 |

| Income for the year before Zakat | 16,444,790 | 11,813,619 | 11,326,358 | 10,135,902 | 9,120,726 |

| Zakat for the year | 1,698,579 | 1,218,071 | 1,167,831 | 6,367,949 | 0 |

| Net income for the year | 14,746,211 | 10,595,548 | 10,158,527 | 3,767,953 | 9,120,726 |

Yield-based operations

Net financing and investment income for the year grew by 21% for the year to SAR 20.4 Bn., accounting to 79% of the total operating income. This was consequent of the strong growth delivered across the retail portfolio including mortgage and personal financing, as well as the growth recorded in the investment portfolio.

Non-yield-based operations

Fees from banking services recorded a 48% growth year-on-year to SAR 5.3 Bn., and accounted for 21% of the total operating income in 2021. Non-yield-based income during the year was driven by improved market share of Al Rajhi Capital in brokerage activities and higher volumes in the stock market as well as expedited migration to cashless payment methods, successfully supported by the Bank’s leading market share in Point-of-Sale (POS) terminals across the Kingdom.

Total operating income

The total operating income of the Bank reached SAR 25.7 Bn. for the year 2021, recording a growth of 24% year-on-year, a result of the strong momentum in the delivery of the BOTF Strategy.

Operating expenses

Multiple initiatives carried out by Al Rajhi Bank over the past few years to optimise cost, digitise products and services, implement latest technologies and improve productivity, collectively impeded the growth of operating expenses to 3% during 2021 to SAR 6.9 Bn. This, coupled with controlled spend and disbursements as well as lowered structural costs among other new initiatives saw the Bank’s Cost-to-Income ratio decrease from 32.5% in 2020 to 26.9% in 2021, an outstanding achievement and a benchmark for the local banking industry.

Impairment charges

The net impairment charge for the year increased by 8% to SAR 2.3 Bn., driven by strong growth delivered across the Bank’s financing portfolio. However, through prudent risk management, the Bank explored growth opportunities without compromising its risk measures, and maintained a healthy balance sheet to decrease its cost of risk from 0.75% in 2020 to 0.60% in 2021.

Profitability

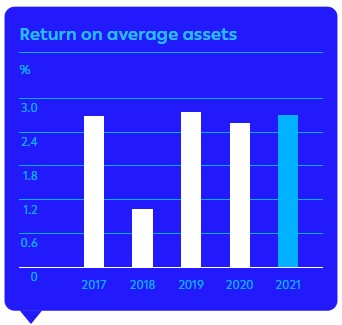

With the increase in net income to SAR 14.7 Bn., earnings per share increased from SAR 4.24 in 2020 to SAR 5.90 in 2021. Return on Assets (ROA) for 2021 increased marginally from 2.56% the previous year to 2.70%, while Return on Equity (ROE) increased from 19.94% to 23.87% year-on-year.

Statement of financial position

Al Rajhi Bank recorded strong growth in assets and liabilities during 2021, maintaining a well-provisioned, healthy balance sheet with greatly improved Non-Performing Loan (NPL) and coverage ratios. With capital funding 11% of total assets during 2021, on-balance sheet gearing remains at a healthy 9.3 times.

Five-year summary of the statement of financial position

| Description | 2021

SAR ’000 |

2020 SAR ’000 |

2019 SAR ’000 |

2018 SAR ’000 |

2017 SAR ’000 |

| Cash and balances with Central Bank “SAMA” and other central banks | 40,363,449 | 47,362,522 | 39,294,099 | 43,246,043 | 48,282,471 |

| Due from banks and other financial institutions, net | 26,065,392 | 28,654,842 | 32,058,182 | 32,387,760 | 10,709,795 |

| Investments, net | 84,433,395 | 60,285,272 | 46,842,630 | 43,062,565 | 36,401,092 |

| Financing, net | 452,830,657 | 315,712,101 | 249,682,805 | 231,758,206 | 233,535,573 |

| Investment properties, net | 1,411,469 | 1,541,211 | 1,383,849 | 1,297,590 | 1,314,006 |

| Property and equipment, net | 10,665,799 | 10,234,785 | 10,407,247 | 8,649,435 | 7,858,127 |

| Other assets, net | 7,901,754 | 5,033,990 | 4,417,764 | 3,629,245 | 5,015,464 |

| Total Assets | 623,671,915 | 468,824,723 | 384,086,576 | 364,030,844 | 343,116,528 |

| Dues to banks and other financial institutions | 17,952,140 | 10,764,061 | 2,219,604 | 7,289,624 | 5,522,567 |

| Customers’ deposits | 512,072,213 | 382,631,003 | 312,405,823 | 293,909,125 | 273,056,445 |

| Other liabilities | 26,338,711 | 17,311,141 | 18,269,492 | 14,526,229 | 8,786,598 |

Total liabilities |

556,363,064 | 410,706,205 | 332,894,919 | 315,724,978 | 287,365,610 |

| Shareholders’ equity | |||||

| Share capital | 25,000,000 | 25,000,000 | 25,000,000 | 16,250,000 | 16,250,000 |

| Statutory reserve | 25,000,000 | 25,000,000 | 21,789,632 | 16,250,000 | 16,250,000 |

| Other reserves | 309,394 | (134,728) | (216,041) | (349,555) | 5,281,682 |

| Retained earnings | 16,999,457 | 8,253,246 | 868,066 | 12,499,171 | 13,906,736 |

| Proposed gross dividends | 0 | 0 | 3,750,000 | 3,656,250 | 4,062,500 |

| Total shareholders’ equity | 67,308,851 | 58,118,518 | 51,191,657 | 48,305,866 | 55,750,918 |

| Total liabilities and shareholders’ equity | 623,671,915 | 468,824,723 | 384,086,576 | 364,030,844 | 343,116,528 |

Assets

Robust growth in business volumes helped Al Rajhi’s asset base to successfully cross SAR 600 Bn. during 2021 to reach SAR 624 Bn. as at 31 December 2021, a growth of 33% compared to 22.1% a year ago. This brings Al Rajhi’s total asset growth over the past five years to 82%.

Financing and investments

Our net financing increased by 43% to SAR 453 Bn., with the overall financing mix remaining predominantly retail, with 81% net exposure. Mortgages made the biggest contribution, having grown by SAR 66 Bn., a year-on-year growth of 63%. Outstanding mortgages amounted to SAR 171 Bn. at the year’s end, representing 46% of the retail portfolio and 37% of the overall financing portfolio. Net investments too increased by 40% to SAR 84 Bn. Over the past five years, the Bank has recorded a financing portfolio growth of 94% and an investment portfolio growth of 132%, contributing to a five-year net income growth of 61.7%.

Asset quality

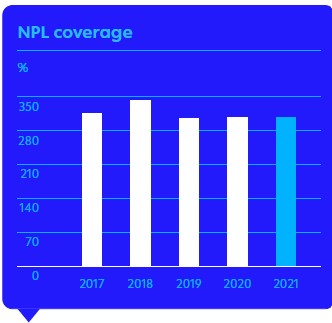

Al Rajhi Bank followed a prudent approach to growth and a conservative approach to provisioning for NPLs, resulting in an improved asset quality during the year with the NPL ratio reducing from 0.76% in 2020 to 0.65% in 2021, the third consecutive year the Bank recorded an improvement on this crucial KPI. The coverage ratio remained above industry average at a healthy 305.6%. As of 2021, 97% of the Bank’s financing portfolio are stage 01 assets, reflecting the Bank’s stringent credit evaluation and post disbursement monitoring process. The remaining 2% and 1% of assets belonged to Stage 2 and Stage 3 respectively. During the year under review, the Bank recorded a coverage rate of 0.83% for Stage 1 assets, with Stage 2 coverage at 24.3% and Stage 3 coverage at 75.6%.

Deposits and other liabilities

Customer deposits increased by SAR 130 Bn. in 2021, a growth of 33.8% to reach SAR 512 Bn. by the year’s end. Demand deposits grew by 12.5% exceeding the average market growth of 6% for the year under review, resulting in improved market share for Al Rajhi. Time deposits also recorded a strong growth in 2021 to fund the overall growth in the financing and investment portfolio.

Stability

A strong and healthy balance sheet in terms of superior asset quality, optimum liquidity and comfortable levels of capital ratios coupled with the support of a loyal shareholder base bears testimony to the stability of Al Rajhi Bank.

Capital

Al Rajhi Bank continued to comfortably maintain a strong capitalisation profile above the regulatory minimum requirements with a Core Equity Tier 1 (CET1) ratio of 16.5%, and total capital adequacy ratio of 17.6% as at 31 December 2021. These ratios were marginally lower than the ratios recorded during the previous year, largely due to a 31.8% increase in Risk-Weighted Assets (RWA) arising primarily from growth in the financing portfolio.

Liquidity

Al Rajhi Bank’s liquidity position remained healthy with a Loan-to-Deposit Ratio (LDR) of 82.3%, a Net Stable Funding Ratio (NSFR) of 114%, and a Liquidity Coverage Ratio (LCR) of 121% supported by High Quality Liquid Assets (HQLA) amounting to SAR 95 Bn. as at 31 December 2021, all within regulatory requirements

Segmental performance

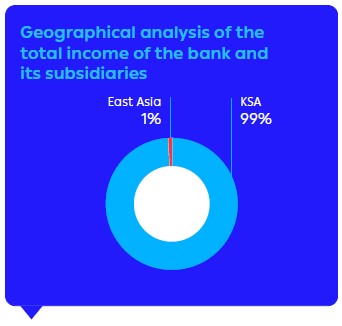

| Geographical analysis of the total income of the bank and its subsidiaries | 2021

SAR ‘000 |

| KSA | 25,514,524 |

| East Asia | 201,874 |

| Total | 25,716,398 |

| Activity Type Revenue | 2021

SAR ‘000 |

| Al Rajhi Capital Company – KSA | 973,352 |

| Tuder Real Estate Company – KSA | 147,261 |

| Al Rajhi Takaful Agency Company – KSA | (1,844) |

| Al Rajhi Company for management services – KSA | 636,182 |

| Emkan Finance Company – KSA | 1,384,196 |

| Tawtheeq Company – KSA | 7,101 |

| Al Rajhi Bank – Jordan | 146,979 |

| Al Rajhi Bank – Kuwait | 112,108 |

| Al Rajhi Corporation Limited – Malaysia | 201,874 |

| International Digital Solutions Co. (Neoleap) | 26,412 |

| Al Rajhi Financial Markets Ltd. | 0 |

| Total | 3,633,621 |

Subsequent events

- On 8 December 2021, the Group entered into a sale and purchase agreement with the shareholders of Ejada Systems Limited Company (“Ejada”) pursuant to which the Group will full acquire the Ejada subject to certain conditions which will be either satisfied or waived in accordance with terms of the agreement. On 16 January 2022, the Group announced that it obtained SAMA’s and General Authority for Competition on the acquisition. The Group has not exercised control on Ejada as of 31 December 2021.

- On 23 January 2022, the Group issued 6,500 Perpetual Sukuk Certificates (Sukuk) of SR 1 Mn. each, and payable quarterly in arrears. The Group has a call option which can be exercised on or after 1 January 2027 as per the terms mentioned in the related offering circular. The expected profit distribution on the Sukuk is the base rate for three months in addition to a profit margin of 3.50%.

- On 16 Rajab 1,443 H (corresponding to 17 February 2022), the bank’s Board of Directors recommended to the Extraordinary General Assembly to increase the bank’s capital from SAR 25,000 Mn. to SAR 40,000 Mn. by granting bonus shares (3 shares for every 5 shares owned). The paid-up capital increase of SAR 15,000 Mn. will be capitalized from retained earnings. The proposed grant is subject to obtaining necessary approvals from official authorities and Extraordinary General Assembly on the capital increase and number of granted shares.

Future outlook

Al Rajhi Bank will continue to focus on its strategic goals shaped by the BOTF strategy, and deliver a financial ecosystem that provides customers with intelligent, innovative financial solutions that address their rapidly evolving needs personal and corporate needs. The Bank will continue to focus on expediting the implementation of digital capabilities across its core retail portfolio, and on attracting high quality corporate portfolios with optimal capital structure to diversify our client base. The SME segment will continue to be one of our key focus areas, with the introduction of improved product offerings as we aim to be the partner in their journey to success. We will also continue to focus on optimising the synergies across our subsidiaries in terms of investments, microfinancing and digital payment solutions among other facilities, to offer the best banking and financial services to our growing customer base.